Cash balance plans have emerged as a solution to many challenges plans face — and they have grown explosively, according to an industry expert in a recent panel discussion. So the timing is right for a refresher on how those plans work, particularly if they occupy an increasingly prominent place in the retirement saving landscape.

That observation came from William Strange, who, like Mike Peatrowsky, is a Principal and Controlling Actuary at Milliman. Joining them in the Sept. 9, 2025 Broadridge webinar “The Power of Cash Balance Plans” was Phil Loftus, a Senior Consulting Actuary at Milliman.

The panelists provided a comprehensive discussion of the basics concerning cash balance plans, how they work, and their importance.

Origins and Developments

Cash balance plans were introduced in the 1980s, panelists noted. They were a less risky, more transparent form of defined benefit plan; however, there was a lack of formal guidance concerning them. Corporate plans and those that were pursuing conversions were their early adopters.

Strange stressed two laws that stand out as especially important to cash balance plans and their increasing prominence. One was the Pension Protection Act (PPA) of 2006, which he said “was where we saw significant interest from professional service firms and small employers.” Milliman says that the PPA confirmed the legitimacy of cash balance plans.

In the wake of the enactment of the PPA, the IRS issued proposed and final regulations concerning cash balance plans in 2010. “We’ve seen explosive growth in cash balance plans” since then, said Strange, and Milliman quantifies it — they report that after 2010, 20,000 new cash balance plans have come into existence.

The second law Strange cited was the SECURE 2.0 Act, which he said includes provisions that are especially important for cash balance plans, especially regarding market-based plans.

Cash Balance Basics

Panelists shared the basics about cash balance plans and how they work, as identified by Milliman.

- Cash balance accounts grow with contributions known as pay credits and interest credits.

- Benefits accrue as a hypothetical account balance throughout a plan participant’s career.

- The selection of pay and interest credits are key design choices; they should reflect the goals of the plan sponsor and meet regulatory and nondiscrimination requirements.

- Payments can be made from a cash balance plan either as a lump sum or as lifetime income.

- Since cash balance contributions are for a DB plan, they are not subject to the DC plan contribution limits.

- Cash balance contributions do not affect what can be contributed to a 401(k) or similar plan.

- Assets are pooled in a single trust. They are managed by professionals, not participants, usually with one asset allocation for the entire pool, although some variations are possible.

- Actual investment experience is passed along to the participant; this reduces the investment risks plan sponsors face.

“Pay and interest credit choices are really the key” regarding cash balance plans and using them, said Peatrowsky.

Cash Balance Q&As

Milliman also provided some questions and answers to give further illustration concerning cash balance plans.

Q: Can the pay credit / contribution ever change for a participant?

A: Yes, they can. They are subject to company review every 3-5 years.

Q: Is there a minimum number of people who must participate in a cash balance plan?

A: Yes. A cash balance plan must have at least 50 participants or 40% of all employees must participate, whichever is lower.

Q: Are cash balance plan accounts portable?

A: Yes. A participant can roll a cash balance plan account over into another employer’s plan or into an IRA to preserve the tax-deferred status.

Q: When can a participant get their money out of a cash balance plan?

A: A participant may take his or her money out of a cash balance plan when he or she leaves the employer that established it, or at age 62, whichever is earlier.

Cash Balance Myths

There are variety of myths surrounding cash balance plans, panelists observed. They provided a sampling of some of them.

Myth: Partners and business owners who are near retirement don’t benefit as much from cash balance plans as do other partners, owners and employees.

Reality: The truth is, said Peatrowsky, that “people who are close to retirement really have the most to gain.” Why? Because (1) they have the highest deferral opportunity, and (2) in-service distributions allow money to be immediately withdrawn, allowing investment direction.

Myth: The federal government and state governments are likely to phase out cash balance plans, given their budget impact.

Reality: There is more of a case to utilize cash balance plans now rather than to regret not taking advantage of their favorable tax treatment while it is available.

Myth: Plan assets are invested too conservatively.

Reality: How the funds of 401(k)s and other investments are handled can help in achieving the risk/return balance one prefers.

Myth: Making a commitment to fully fund a 401(k) Profit Sharing plan puts a strain on cash flow strained.

Reality: For partners/owners concerned about cash flow, always an option to dial back 401(k) contribution to offset cash balance contribution.

Myth: If a cash balance fund has a negative return in year 1, we will have to contribute the difference.

Reality: This will only be necessary when someone retires or otherwise becomes eligible to take a lump sum, and chooses to take a distribution.

Myth: If a cash balance fund has a negative return in year 5, it will be necessary to make up the difference for any retiring owner.

Reality: That is not necessarily the case. If the amount of the loss in year 5 is less than the sum of gains in years 1-4 and the participant takes their benefit, their cumulative return is greater than 0% and it will not be necessary to do so.

Myth: Investment volatility will increase the likelihood of wealth transfer between owners.

Reality: Investment strategy is professionally managed and generally conservative, which reduces the likelihood of a sustained losses — especially over longer periods.

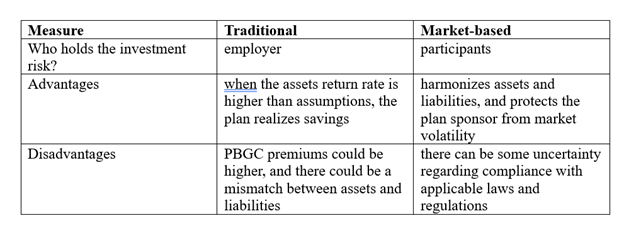

Tomato, Tomahto

How do cash balance plans differ, based on how they are invested? And are there differences between the two regarding how they perform when they are invested in different ways?

Milliman provides an illustration of the differences between a traditional cash balance plan connected to bond yields and the other a market-based cash balance plan.

October Three conducted a study of the performance of two hypothetical cash balance plans — one a traditional cash balance plan and the other a market-based cash balance plan — during the period 2021-2024.

The traditional plan provides interest credits connected to 30-year Treasury yields, while the market-based plan is invested in a 2030 target date fund portfolio.

October Three says that its hypothetical traditional cash balance plan performed better than its market-based counterpart from spring of 2021 through fall 2023, with rough parity between the two from late 2023 through spring 2024. Since late spring of 2024, the market-based cash balance plan has performed better.

Drilling down, October Three reports that in three out of the four years in the study period, the market-based cash balance plan outperformed that traditional plan regarding the real monthly retirement income they generated.

2021: Market-based plan, +6%; traditional plan, -3%

2022: Market-based plan, +9%; traditional plan, +32%

2023: Market-based plan, +9%; traditional plan, +2%

2024: Market-based plan, +6%; traditional plan, 0%

October Three attributes the steady growth of the market-based plan to the ability of equities to offset the effects of inflation; it said the “windfall gain” the traditional plan enjoyed in 2022 was due to a “sharp increase in interest rates we saw that year.”

Why?

So why would a retirement plan professionals suggest that a plan sponsor offer a cash balance plan to its employees? Panelists offer some ideas.

They argued that growth in assets can be rapid, depending on the size of the deferrals. They further suggested that retirement plan professionals that present clients and prospective clients with the option of adopting a cash balance plan not only may expand their client base, they also demonstrate their effort to make them aware of available options and help them expand their plan offerings.